n our last Strategic Insights, we analyzed the impact of President Trump’s global tariff war. We concluded that history suggests the S&P 500 is at best priced for modest 5%type returns. It could undergo a more severe setback if things do not break the way the bulls are hoping.

The S&P 500 has reached a point where it can chug along for several years posting modest gains, or it can suffer a significant selloff. We cannot determine which outcome is more likely. With that as a backdrop, we will attempt to find a strategy that investors can adopt in this environment.

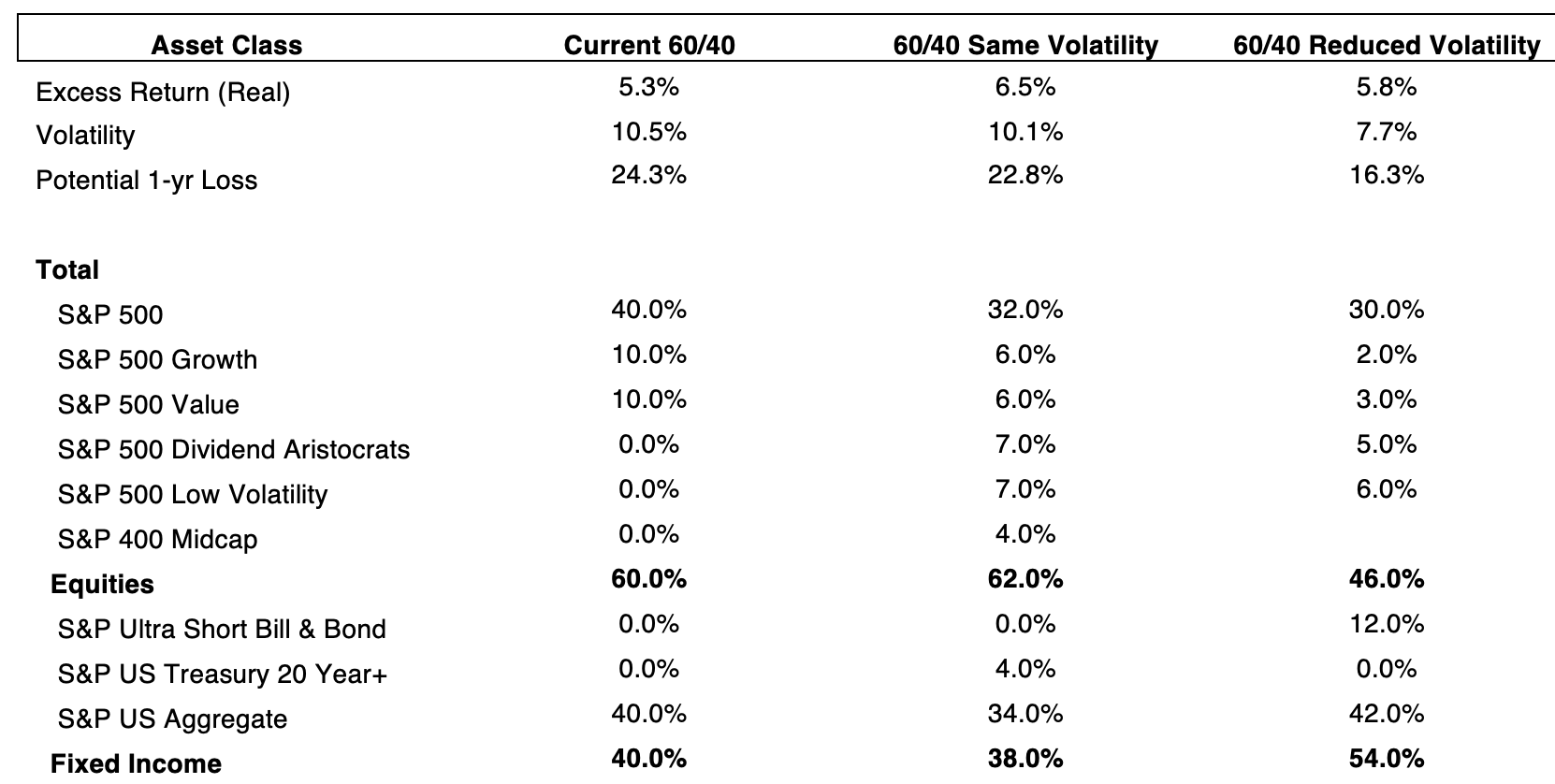

We will draw up two stratigies for the standard 60/40 portfolio model. One is built to thrive in a 5% S&P world. The other far more conservative portfolio option is designed to survive a more dramatic revaluation. Investors can modify the 60/40 portfolios to account for higher initial equity weights such as an 80/20 or a 100% equity weights.

We have devised two portfolio modifications to a 60/40 model. The first model consists of a comparable risk to the original model while the second model reduces portfolio risk by about one fourth based on volatility and about one third based upon one year downside. These models assume 100% US equities, but global portfolios can make similar adjustments to US equity weightings and arrive at similar risk levels.

The comparable risk model drops model weighting in the S&P 500, S&P 500 Growth and S&P 500 Value asset classes. Theses asset classes are overvalued based on their distance from trend. For example, the largest stock in the S&P 500 is NVIDIA at over 8% of the S&P, and the Magnificent 7 of highly valued growth stocks is trading at 1.3x sales.

The weighting of these overvalued asset classes has been moved to S&P DividendAristocrats, S&P Low Volatility, and S&P 400 Midcap. We took over all equity weighting up 2% to maintain comparable risk to the original model, since the Dividend and Low Volatility asset classes have less risk than the asset classes with which they were exchanged. We also exchanged 4% of Fixed Income weighting to long treasury bonds, as represented by the S&P US Treasury 20 Year+ index. This new 60/40 model has slightly less risk that the existing model but is positioned for outperformance should undervalued asset classes begin to pick up their performance.

The second 60/40 model is designed for the inevitable reckoning that every overvalued market eventually takes. The broad themes of this model are like those of the comparable risk model, but the weightings are different to take into account the need to reduce overall risk. The overvalued S&P 500, S&P 500 Growth and S&P 500 Value are reduced even more that in the Comparable risk model. These adjustments are not fully made up by increased weighting in the undervalued Dividend Aristocrats and LowVolatility, and no assets were deployed into Midcap. A fixed income weighting was created in cash equivalents (Ultra Short T-bill & Bond) to soak up excess cash in a very low risk way.

Caravel Concept has deliberately put out two models because frankly we are torn. We could easily see the market continue to run at a slower pace for several more years, as it did in the 1960’s. However, we have ultimately decided to embrace the lower risk model. The S&P 500 is extremely overvalued and the Magnificent 7 are emblematic of overvalued stocks of the past. We see little reason for a major equity market pull back other than the price of the most overvalued sectors of the market. When confronted with an overvalued market, our instinct is to get cautious, build cash, and wait for things to settle down and return to normal.

Opinions expressed are current as of the date shown and are subject to change. They are not intended as investment recommendations.

Past results are no guarantee of future results and no representation is made that an investor will or is likely to achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Diversification does not ensure a profit or protect against a loss.

Institutional Brokers’ Estimate System (IBES) is a database that gathers and compiles the different estimates made by stock analysts on the future earnings for the majority of U.S. publicly traded companies.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e, the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Strategies seeking higher returns generally have a greater allocation to equities. These strategies also carry higher risks and are subject to a greater degree of market volatility.

Using a currency hedge or a currency hedged product does not insulate the portfolio against losses.

Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability.

Inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Small-, mid- and micro-cap companies may be hindered as a result of limited resources or less diverse products or services and have therefore historically been more volatile than the stocks of larger, more established companies.

In a rising interest rate environment, the value of fixed-income securities generally declines.

High-yield securities (including junk bonds) are subject to greater risk of loss of principal and interest, including default risk, than higher rated securities.

Copyright ©2025 Caravel Concepts, LLC. All rights reserved.